Debt-to-Income Ratio: Why it’s Important

When it comes to getting a mortgage, many people think that their credit scores are the most important numbers that are associated with their names. While a person’s credit score is important, along with how much money they have saved, there’s another number that is just as important: their debt-to-income (DTI) ratio.

A DTI ratio is one of the ways lenders measure your ability to make payments toward money you’ve borrowed. Your DTI ratio is expressed as a percentage and is comprised of your total minimum monthly debt divided by your gross (before tax) monthly income. Your total minimum monthly debt is made up of your minimum monthly payments for car loans, student loans, credit card debt, home equity loans, mortgages, and any other recurring debt you might have.

When you’re in the market for a mortgage, it’s imperative that you know your DTI. To calculate it, you must take into account all of your monthly debt payments and divide the total by your gross monthly income (the amount of money you earn before taxes). For example, if you pay $1,500 a month for your mortgage, $100 a month for an auto loan and $400 a month for the rest of your debts, you pay a total of $2,000 per month toward debts. If your gross monthly income is $6,000, then your DTI ratio is 33%.

It’s important to remember that your minimum monthly debt is the minimum you are required to pay each month. For example, if you owe $3,000 on a high-interest credit card, and your minimum payment on that specific card is $150, only that $150 is going to figure into your DTI. Keep in mind, however, that paying only the minimum amount on your debts can make them grow larger.

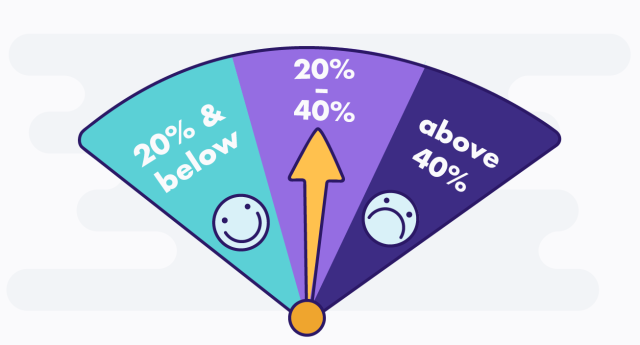

A good rule of thumb is the lower your DTI, the better. A DTI less than 50% is generally considered workable in the mortgage industry. However, if your DTI is higher than 50%, you may have a difficult time qualifying for a mortgage. If your DTI is 20% or lower, you’ll be able to borrow more and have more options than someone with a higher DTI.

If your DTI isn’t to your liking, you’ve got two options, both of which are easier said than done. Your first option is to increase your income so you have more money to work with. Your second option is to reduce your debts to enable your existing income to go further. For the second option, focus on paying off your credit cards and other loans, and avoid taking on additional debts.

If you’re in the market for a new mortgage, don’t overlook your DTI. Many people assume that if they have a good credit score and good income, getting a mortgage will be no problem. The fact is that a good DTI also has a huge impact on getting you qualified for a mortgage.

Posted by: Carlson Mortgage – a top-rated St. Louis mortgage broker providing home loans in the state of Missouri. We are routinely ranked as a #1 mortgage broker in Missouri on Yelp, Google and Zillow. We can be reached at (314) 329-7314 seven days a week.

Our loan application can be found here or you can call us at 314-329-7314 to speak with one of our mortgage loan officers. Also, here is our pre-approval page, if you are looking to buy a home or need a referral to a top real estate agent.

Let us be your source for some of the lowest mortgage interest rates in St. Louis on first-time home buyer, conventional, FHA, Veterans (VA), Jumbo and condominium (condo) financing. Since 2004, we’ve been providing home loans and mortgage services in St. Louis that are tailored individually to your unique needs and to your financial situation. Our loan officers speak English, Spanish and Russian. Call us today to inquire about home loan interest rates, to get pre-approved for a purchase or a refinance mortgage, or if you have any general mortgage lending questions.